Enhanced Scalping IndicatorEnhanced Scalping Indicator - Professional Multi-Confirmation Trading System

Overview

The Enhanced Scalping Indicator is a sophisticated trading tool designed for short-term traders seeking high-probability entry and exit signals. This indicator combines multiple technical analysis techniques with adaptive market conditions to filter noise and identify optimal trading opportunities.

Key Features

🎯 Multi-Confirmation Signal System

- Enhanced RSI with Adaptive Thresholds: Dynamic overbought/oversold levels that adjust based on market volatility (ATR)

- Higher Timeframe Confirmation: Uses 1-hour RSI to validate signals from lower timeframes

- Volume-Weighted Momentum: Incorporates volume analysis to confirm price movements

- Market Structure Analysis: Evaluates price position within recent 20-bar range

📊 Advanced Signal Generation

- Buy Signals: Triggered when RSI is oversold with upward momentum, confirmed by higher timeframe bearish conditions and strong volume

- Sell Signals: Activated when RSI is overbought with downward momentum, validated by higher timeframe bullish conditions and high volume

- Exit Signals: Smart exit conditions based on RSI mean reversion and momentum shifts

🔄 Divergence Detection (Optional)

- Bullish Divergence: Identifies when price makes lower lows while RSI makes higher lows

- Bearish Divergence: Spots when price makes higher highs while RSI makes lower highs

- Volume Confirmation: All divergence signals require above-average volume for validation

⚙️ Customizable Parameters

- RSI Settings: Adjustable length (default: 14) and source

- Moving Average Options: Choose from SMA, EMA, SMMA, WMA, VWMA, or Bollinger Bands

- Higher Timeframe: Configurable confirmation timeframe (default: 1 hour)

- ATR Period: [

/b] Volatility measurement period for adaptive thresholds

📈 Visual Elements

- Dynamic Threshold Lines: Adaptive overbought/oversold levels

- Signal Shapes: Clear buy/sell and exit signals on chart

- Background Highlighting: Color-coded background for active signals

- Real-time Information Table: Displays current RSI, higher timeframe RSI, volatility ratio, market position, and momentum

🚨 Alert System

Complete alert functionality for:

- Enhanced buy signals

- Enhanced sell signals

- Long position exits

- Short position exits

Best Use Cases

- Scalping: 1-5 minute timeframes for quick trades

- Day Trading: 15-30 minute timeframes for intraday positions

- Swing Trading: Higher timeframes with divergence detection enabled

Market Conditions

Works effectively in:

- T rending Markets: Momentum and higher timeframe filters reduce false signals

- Range-bound Markets: Adaptive thresholds adjust to market volatility

- High Volume Sessions: Built-in volume filters ensure signal quality

Strategy Integration

This indicator works well with:

- Support/resistance levels

- Price action analysis

- Risk management rules (stop losses, position sizing)

- Market session awareness (built-in US market hours filter)

Technical Implementation

- Built on Pine Script v6

- Utilizes proper RMA calculations for RSI

- Implements consistent historical data access

- Optimized for performance with minimal repainting

Risk Disclaimer

This indicator is a technical analysis tool and should not be used as the sole basis for trading decisions. Always combine with proper risk management, fundamental analysis, and your trading strategy. Past performance does not guarantee future results.

---

Perfect for: Scalpers, day traders, and swing traders looking for a comprehensive, multi-confirmation trading system with built-in risk management features.

Cari dalam skrip untuk "swing trading"

Enhanced Stock Ticker with 50MA vs 200MADescription

The Enhanced Stock Ticker with 50MA vs 200MA is a versatile Pine Script indicator designed to visualize the relative position of a stock's price within its short-term and long-term price ranges, providing actionable bullish and bearish signals. By calculating normalized indices based on user-defined lookback periods (defaulting to 50 and 200 bars), this indicator helps traders identify potential reversals or trend continuations. It offers the flexibility to plot signals either on the main price chart or in a separate lower pane, leveraging Pine Script v6's force_overlay functionality for seamless integration. The indicator also includes a customizable ticker table, visual fills, and alert conditions for automated trading setups.

Key Features

Dual Lookback Indices: Computes short-term (default: 50 bars) and long-term (default: 200 bars) indices, normalizing the closing price relative to the high/low range over the specified periods.

Flexible Signal Plotting: Users can toggle between plotting crossover signals (triangles) on the main price chart (location.abovebar/belowbar) or in the lower pane (location.top/bottom) using the Plot Signals on Main Chart option.

Crossover Signals: Generates bullish (Golden Cross) and bearish (Death Cross) signals when the short or long index crosses above 5 or below 95, respectively.

Visual Enhancements:

Plots short-term (blue) and long-term (white) indices in a separate pane with customizable lookback periods.

Includes horizontal reference lines at 0, 20, 50, 80, and 100, with green and red fills to highlight overbought/oversold zones.

Dynamic fill between indices (green when short > long, red when long > short) for quick trend visualization.

Displays a ticker and legend table in the top-right corner, showing the symbol and lookback periods.

Alert Conditions: Supports alerts for bullish and bearish crossovers on both short and long indices, enabling integration with TradingView's alert system.

Technical Innovation: Utilizes Pine Script v6's force_overlay parameter to plot signals on the main chart from a non-overlay indicator, combining the benefits of a separate pane and chart-based signals in a single script.

Technical Details

Calculation Logic:

Uses confirmed bars (barstate.isconfirmed) to calculate indices, ensuring reliability by avoiding real-time bar fluctuations.

Short-term index: (close - lowest(low, lookback_short)) / (highest(high, lookback_short) - lowest(low, lookback_short)) * 100

Long-term index: (close - lowest(low, lookback_long)) / (highest(high, lookback_long) - lowest(low, lookback_long)) * 100

Signals are triggered using ta.crossover() and ta.crossunder() for indices crossing 5 (bullish) and 95 (bearish).

Signal Plotting:

Main chart signals use force_overlay=true with location.abovebar/belowbar for precise alignment with price bars.

Lower pane signals use location.top/bottom for visibility within the indicator pane.

Plotting is controlled by boolean conditions (e.g., bullishLong and plot_on_chart) to ensure compliance with Pine Script's global scope requirements.

Performance Considerations: Optimized for efficiency by calculating indices only on confirmed bars and using lightweight plotting functions.

How to Use

Add to Chart:

Copy the script into TradingView's Pine Editor and add it to your chart.

Configure Settings:

Short Lookback Period: Adjust the short-term lookback (default: 50 bars) to match your trading style (e.g., 20 for shorter-term analysis).

Long Lookback Period: Adjust the long-term lookback (default: 200 bars) for broader market context.

Plot Signals on Main Chart: Check this box to display signals on the price chart; uncheck to show signals in the lower pane.

Interpret Signals:

Golden Cross (Bullish): Green (long) or blue (short) triangles indicate the index crossing above 5, suggesting a potential buying opportunity.

Death Cross (Bearish): Red (long) or white (short) triangles indicate the index crossing below 95, signaling a potential selling opportunity.

Set Alerts:

Use TradingView's alert system to create notifications for the four alert conditions: Long Index Valley, Long Index Peak, Short Index Valley, and Short Index Peak.

Customize Visuals:

The ticker table displays the symbol and lookback periods in the top-right corner.

Adjust colors and styles via TradingView's settings if desired.

Example Use Cases

Swing Trading: Use the short-term index (e.g., 50 bars) to identify short-term reversals within a broader trend defined by the long-term index.

Trend Confirmation: Monitor the fill between indices to confirm whether the short-term trend aligns with the long-term trend.

Automated Trading: Leverage alert conditions to integrate with bots or manual trading strategies.

Notes

Testing: Always backtest the indicator on your chosen market and timeframe to validate its effectiveness.

Optional Histogram: The script includes a commented-out histogram for the index difference (index_short - index_long). Uncomment the plot(index_diff, ...) line to enable it.

Compatibility: Built for Pine Script v6 and tested on TradingView as of May 27, 2025.

Acknowledgments

This indicator was inspired by the need for a flexible tool that combines lower-pane analysis with main chart signals, made possible by Pine Script's force_overlay feature. Share your feedback or suggestions in the comments below, and happy trading!

Ergodic Market Divergence (EMD)Ergodic Market Divergence (EMD)

Bridging Statistical Physics and Market Dynamics Through Ensemble Analysis

The Revolutionary Concept: When Physics Meets Trading

After months of research into ergodic theory—a fundamental principle in statistical mechanics—I've developed a trading system that identifies when markets transition between predictable and unpredictable states. This indicator doesn't just follow price; it analyzes whether current market behavior will persist or revert, giving traders a scientific edge in timing entries and exits.

The Core Innovation: Ergodic Theory Applied to Markets

What Makes Markets Ergodic or Non-Ergodic?

In statistical physics, ergodicity determines whether a system's future resembles its past. Applied to trading:

Ergodic Markets (Mean-Reverting)

- Time averages equal ensemble averages

- Historical patterns repeat reliably

- Price oscillates around equilibrium

- Traditional indicators work well

Non-Ergodic Markets (Trending)

- Path dependency dominates

- History doesn't predict future

- Price creates new equilibrium levels

- Momentum strategies excel

The Mathematical Framework

The Ergodic Score combines three critical divergences:

Ergodic Score = (Price Divergence × Market Stress + Return Divergence × 1000 + Volatility Divergence × 50) / 3

Where:

Price Divergence: How far current price deviates from market consensus

Return Divergence: Momentum differential between instrument and market

Volatility Divergence: Volatility regime misalignment

Market Stress: Adaptive multiplier based on current conditions

The Ensemble Analysis Revolution

Beyond Single-Instrument Analysis

Traditional indicators analyze one chart in isolation. EMD monitors multiple correlated markets simultaneously (SPY, QQQ, IWM, DIA) to detect systemic regime changes. This ensemble approach:

Reveals Hidden Divergences: Individual stocks may diverge from market consensus before major moves

Filters False Signals: Requires broader market confirmation

Identifies Regime Shifts: Detects when entire market structure changes

Provides Context: Shows if moves are isolated or systemic

Dynamic Threshold Adaptation

Unlike fixed-threshold systems, EMD's boundaries evolve with market conditions:

Base Threshold = SMA(Ergodic Score, Lookback × 3)

Adaptive Component = StDev(Ergodic Score, Lookback × 2) × Sensitivity

Final Threshold = Smoothed(Base + Adaptive)

This creates context-aware signals that remain effective across different market environments.

The Confidence Engine: Know Your Signal Quality

Multi-Factor Confidence Scoring

Every signal receives a confidence score based on:

Signal Clarity (0-35%): How decisively the ergodic threshold is crossed

Momentum Strength (0-25%): Rate of ergodic change

Volatility Alignment (0-20%): Whether volatility supports the signal

Market Quality (0-20%): Price convergence and path dependency factors

Real-Time Confidence Updates

The Live Confidence metric continuously updates, showing:

- Current opportunity quality

- Market state clarity

- Historical performance influence

- Signal recency boost

- Visual Intelligence System

Adaptive Ergodic Field Bands

Dynamic bands that expand and contract based on market state:

Primary Color: Ergodic state (mean-reverting)

Danger Color: Non-ergodic state (trending)

Band Width: Expected price movement range

Squeeze Indicators: Volatility compression warnings

Quantum Wave Ribbons

Triple EMA system (8, 21, 55) revealing market flow:

Compressed Ribbons: Consolidation imminent

Expanding Ribbons: Directional move developing

Color Coding: Matches current ergodic state

Phase Transition Signals

Clear entry/exit markers at regime changes:

Bull Signals: Ergodic restoration (mean reversion opportunity)

Bear Signals: Ergodic break (trend following opportunity)

Confidence Labels: Percentage showing signal quality

Visual Intensity: Stronger signals = deeper colors

Professional Dashboard Suite

Main Analytics Panel (Top Right)

Market State Monitor

- Current regime (Ergodic/Non-Ergodic)

- Ergodic score with threshold

- Path dependency strength

- Quantum coherence percentage

Divergence Metrics

- Price divergence with severity

- Volatility regime classification

- Strategy mode recommendation

- Signal strength indicator

Live Intelligence

- Real-time confidence score

- Color-coded risk levels

- Dynamic strategy suggestions

Performance Tracking (Left Panel)

Signal Analytics

- Total historical signals

- Win rate with W/L breakdown

- Current streak tracking

- Closed trade counter

Regime Analysis

- Current market behavior

- Bars since last signal

- Recommended actions

- Average confidence trends

Strategy Command Center (Bottom Right)

Adaptive Recommendations

- Active strategy mode

- Primary approach (mean reversion/momentum)

- Suggested indicators ("weapons")

- Entry/exit methodology

- Risk management guidance

- Comprehensive Input Guide

Core Algorithm Parameters

Analysis Period (10-100 bars)

Scalping (10-15): Ultra-responsive, more signals, higher noise

Day Trading (20-30): Balanced sensitivity and stability

Swing Trading (40-100): Smooth signals, major moves only Default: 20 - optimal for most timeframes

Divergence Threshold (0.5-5.0)

Hair Trigger (0.5-1.0): Catches every wiggle, many false signals

Balanced (1.5-2.5): Good signal-to-noise ratio

Conservative (3.0-5.0): Only extreme divergences Default: 1.5 - best risk/reward balance

Path Memory (20-200 bars)

Short Memory (20-50): Recent behavior focus, quick adaptation

Medium Memory (50-100): Balanced historical context

Long Memory (100-200): Emphasizes established patterns Default: 50 - captures sufficient history without lag

Signal Spacing (5-50 bars)

Aggressive (5-10): Allows rapid-fire signals

Normal (15-25): Prevents clustering, maintains flow

Conservative (30-50): Major setups only Default: 15 - optimal trade frequency

Ensemble Configuration

Select markets for consensus analysis:

SPY: Broad market sentiment

QQQ: Technology leadership

IWM: Small-cap risk appetite

DIA: Blue-chip stability

More instruments = stronger consensus but potentially diluted signals

Visual Customization

Color Themes (6 professional options):

Quantum: Cyan/Pink - Modern trading aesthetic

Matrix: Green/Red - Classic terminal look

Heat: Blue/Red - Temperature metaphor

Neon: Cyan/Magenta - High contrast

Ocean: Turquoise/Coral - Calming palette

Sunset: Red-orange/Teal - Warm gradients

Display Controls:

- Toggle each visual component

- Adjust transparency levels

- Scale dashboard text

- Show/hide confidence scores

- Trading Strategies by Market State

- Ergodic State Strategy (Primary Color Bands)

Market Characteristics

- Price oscillates predictably

- Support/resistance hold

- Volume patterns repeat

- Mean reversion dominates

Optimal Approach

Entry: Fade moves at band extremes

Target: Middle band (equilibrium)

Stop: Just beyond outer bands

Size: Full confidence-based position

Recommended Tools

- RSI for oversold/overbought

- Bollinger Bands for extremes

- Volume profile for levels

- Non-Ergodic State Strategy (Danger Color Bands)

Market Characteristics

- Price trends persistently

- Levels break decisively

- Volume confirms direction

- Momentum accelerates

Optimal Approach

Entry: Breakout from bands

Target: Trail with expanding bands

Stop: Inside opposite band

Size: Scale in with trend

Recommended Tools

- Moving average alignment

- ADX for trend strength

- MACD for momentum

- Advanced Features Explained

Quantum Coherence Metric

Measures phase alignment between individual and ensemble behavior:

80-100%: Perfect sync - strong mean reversion setup

50-80%: Moderate alignment - mixed signals

0-50%: Decoherence - trending behavior likely

Path Dependency Analysis

Quantifies how much history influences current price:

Low (<30%): Technical patterns reliable

Medium (30-50%): Mixed influences

High (>50%): Fundamental shift occurring

Volatility Regime Classification

Contextualizes current volatility:

Normal: Standard strategies apply

Elevated: Widen stops, reduce size

Extreme: Defensive mode required

Signal Strength Indicator

Real-time opportunity quality:

- Distance from threshold

- Momentum acceleration

- Cross-validation factors

Risk Management Framework

Position Sizing by Confidence

90%+ confidence = 100% position size

70-90% confidence = 75% position size

50-70% confidence = 50% position size

<50% confidence = 25% or skip

Dynamic Stop Placement

Ergodic State: ATR × 1.0 from entry

Non-Ergodic State: ATR × 2.0 from entry

Volatility Adjustment: Multiply by current regime

Multi-Timeframe Alignment

- Check higher timeframe regime

- Confirm ensemble consensus

- Verify volume participation

- Align with major levels

What Makes EMD Unique

Original Contributions

First Ergodic Theory Trading Application: Transforms abstract physics into practical signals

Ensemble Market Analysis: Revolutionary multi-market divergence system

Adaptive Confidence Engine: Institutional-grade signal quality metrics

Quantum Coherence: Novel market alignment measurement

Smart Signal Management: Prevents clustering while maintaining responsiveness

Technical Innovations

Dynamic Threshold Adaptation: Self-adjusting sensitivity

Path Memory Integration: Historical dependency weighting

Stress-Adjusted Scoring: Market condition normalization

Real-Time Performance Tracking: Built-in strategy analytics

Optimization Guidelines

By Timeframe

Scalping (1-5 min)

Period: 10-15

Threshold: 0.5-1.0

Memory: 20-30

Spacing: 5-10

Day Trading (5-60 min)

Period: 20-30

Threshold: 1.5-2.5

Memory: 40-60

Spacing: 15-20

Swing Trading (1H-1D)

Period: 40-60

Threshold: 2.0-3.0

Memory: 80-120

Spacing: 25-35

Position Trading (1D-1W)

Period: 60-100

Threshold: 3.0-5.0

Memory: 100-200

Spacing: 40-50

By Market Condition

Trending Markets

- Increase threshold

- Extend memory

- Focus on breaks

Ranging Markets

- Decrease threshold

- Shorten memory

- Focus on restores

Volatile Markets

- Increase spacing

- Raise confidence requirement

- Reduce position size

- Integration with Other Analysis

- Complementary Indicators

For Ergodic States

- RSI divergences

- Bollinger Band squeezes

- Volume profile nodes

- Support/resistance levels

For Non-Ergodic States

- Moving average ribbons

- Trend strength indicators

- Momentum oscillators

- Breakout patterns

- Fundamental Alignment

- Check economic calendar

- Monitor sector rotation

- Consider market themes

- Evaluate risk sentiment

Troubleshooting Guide

Too Many Signals:

- Increase threshold

- Extend signal spacing

- Raise confidence minimum

Missing Opportunities

- Decrease threshold

- Reduce signal spacing

- Check ensemble settings

Poor Win Rate

- Verify timeframe alignment

- Confirm volume participation

- Review risk management

Disclaimer

This indicator is for educational and informational purposes only. It does not constitute financial advice. Trading involves substantial risk of loss and is not suitable for all investors. Past performance does not guarantee future results.

The ergodic framework provides unique market insights but cannot predict future price movements with certainty. Always use proper risk management, conduct your own analysis, and never risk more than you can afford to lose.

This tool should complement, not replace, comprehensive trading strategies and sound judgment. Markets remain inherently unpredictable despite advanced analysis techniques.

Transform market chaos into trading clarity with Ergodic Market Divergence.

Created with passion for the TradingView community

Trade with insight. Trade with anticipation.

— Dskyz , for DAFE Trading Systems

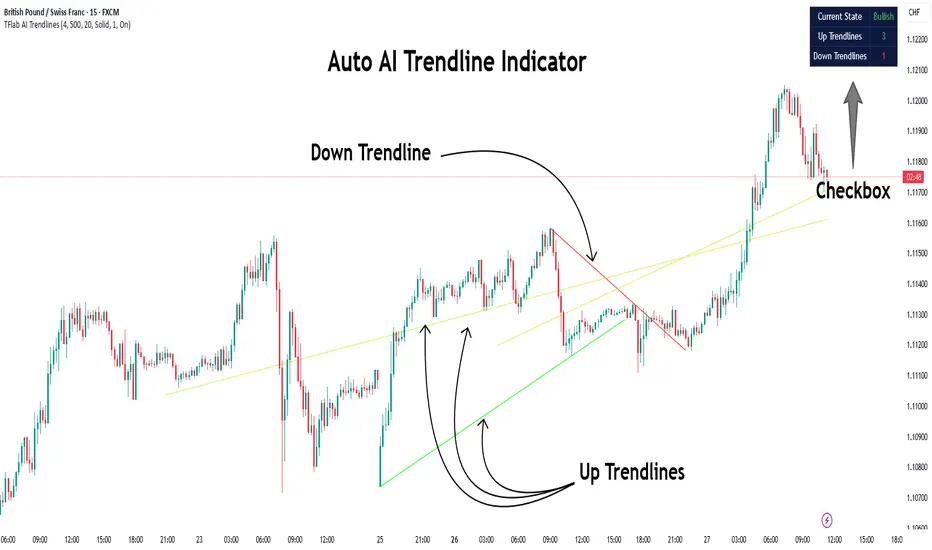

Auto AI Trendlines [TradingFinder] Clustering & Filtering Trends🔵 Introduction

Auto AI trendlines Clustering & Filtering Trends Indicator, draws a variety of trendlines. This auto plotting trendline indicator plots precise trendlines and regression lines, capturing trend dynamics.

Trendline trading is the strongest strategy in the financial market.

Regression lines, unlike trendlines, use statistical fitting to smooth price data, revealing trend slopes. Trendlines connect confirmed pivots, ensuring structural accuracy. Regression lines adapt dynamically.

The indicator’s ascending trendlines mark bullish pivots, while descending ones signal bearish trends. Regression lines extend in steps, reflecting momentum shifts. As the trend is your friend, this tool aligns traders with market flow.

Pivot-based trendlines remain fixed once confirmed, offering reliable support and resistance zones. Regression lines, adjusting to price changes, highlight short-term trend paths. Both are vital for traders across asset classes.

🔵 How to Use

There are four line types that are seen in the image below; Precise uptrend (green) and downtrend (red) lines connect exact price extremes, while Pivot-based uptrend and downtrend lines use significant swing points, both remaining static once formed.

🟣 Precise Trendlines

Trendlines only form after pivot points are confirmed, ensuring reliability. This reduces false signals in choppy markets. Regression lines complement with real-time updates.

The indicator always draws two precise trendlines on confirmed pivot points, one ascending and one descending. These are colored distinctly to mark bullish and bearish trends. They remain fixed, serving as structural anchors.

🟣 Dynamic Regression Lines

Regression lines, adjusting dynamically with price, reflect the latest trend slope for real-time analysis. Use these to identify trend direction and potential reversals.

Regression lines, updated dynamically, reflect real-time price trends and extend in steps. Ascending lines are green, descending ones orange, with shades differing from trendlines. This aids visual distinction.

🟣 Bearish Chart

A Bullish State emerges when uptrend lines outweigh or match downtrend lines, with recent upward momentum signaling a potential rise. Check the trend count in the state table to confirm, using it to plan long positions.

🟣 Bullish Chart

A Bearish State is indicated when downtrend lines dominate or equal uptrend lines, with recent downward moves suggesting a potential drop. Review the state table’s trend count to verify, guiding short position entries. The indicator reflects this shift for strategic planning.

🟣 Alarm

Set alerts for state changes to stay informed of Bullish or Bearish shifts without constant monitoring. For example, a transition to Bullish State may signal a buying opportunity. Toggle alerts On or Off in the settings.

🟣 Market Status

A table summarizes the chart’s status, showing counts of ascending and descending lines. This real-time overview simplifies trend monitoring. Check it to assess market bias instantly.

Monitor the table to track line counts and trend dominance.

A higher count of ascending lines suggests bullish bias. This helps traders align with the prevailing trend.

🔵 Settings

Number of Trendlines : Sets total lines (max 10, min 3), balancing chart clarity and trend coverage.

Max Look Back : Defines historical bars (min 50) for pivot detection, ensuring robust trendlines.

Pivot Range : Sets pivot sensitivity (min 2), adjusting trendline precision to market volatility.

Show Table Checkbox : Toggles display of a table showing ascending/descending line counts.

Alarm : Enable or Disable the alert.

🔵 Conclusion

The multi slopes indicator, blending pivot-based trendlines and dynamic regression lines, maps market trends with precision. Its dual approach captures both structural and short-term momentum.

Customizable settings, like trendline count and pivot range, adapt to diverse trading styles. The real-time table simplifies trend monitoring, enhancing efficiency. It suits forex, stocks, and crypto markets.

While trendlines anchor long-term trends, regression lines track intraday shifts, offering versatility. Contextual analysis, like price action, boosts signal reliability. This indicator empowers data-driven trading decisions.

Multi-Timeframe MA Breakout/Breakdown Analysis📊 Overview

This sophisticated Pine Script indicator revolutionizes breakout/breakdown analysis by distinguishing between fake and genuine signals using a unique swing-level validation methodology. Unlike traditional moving average crossovers, this system validates price movements against historical swing points, providing traders with high-probability entry and exit signals across multiple timeframes.

🎯 Core Trading Methodology

The Swing Validation Concept:

Traditional MA breakouts often fail because they don't consider the context of previous price action. This indicator solves this by:

Recording swing levels when each MA is initially crossed

Validating subsequent crosses against these historical swing points

Classifying signals as fake or genuine based on this validation

Tracking signal evolution as price action develops

Signal Classification System:

🔻 Breakdown Analysis:

Fake Breakdown: Price cuts below MA but stays above the swing low from previous MA cut

Genuine Breakdown: Price cuts below MA and falls below the swing low from previous MA cut

Validation Chain: EMA 50 validates against EMA 20 swing low, EMA 100 against EMA 50 swing low, EMA 200 against EMA 100 swing low

🔺 Breakout Analysis:

Fake Breakout: Price crosses above MA but stays below the swing high from previous MA cross

Genuine Breakout: Price crosses above MA and exceeds the swing high from previous MA cross

Validation Chain: EMA 50 validates against EMA 20 swing high, EMA 100 against EMA 50 swing high, EMA 200 against EMA 100 swing high

📈 Signal Interpretation Guide

Visual Chart Signals:

Breakdown Signals:

🔻 Orange Triangle Down + "FAKE BREAKDOWN": Potential reversal opportunity - price likely to bounce

🔻 Red Triangle Down + "GENUINE BREAKDOWN": Trend continuation - expect further downside

🔺 Lime Triangle Up + "BULLISH REVERSAL": Strong buy signal after fake breakdown validation

Breakout Signals:

🔺 Orange Triangle Up + "FAKE BREAKOUT": Potential reversal opportunity - price likely to decline

🔺 Dark Red Triangle Up + "GENUINE BREAKOUT": Trend continuation - expect further upside

🔻 Fuchsia Triangle Down + "BEARISH REVERSAL": Strong sell signal after fake breakout validation

Multi-Timeframe Analysis Table:

Signal Column Interpretation:

"FAKE BD" (Orange): Fake breakdown detected - watch for bullish reversal

"GENUINE BD" (Red): Genuine breakdown - bearish continuation likely

"FAKE BO" (Orange): Fake breakout detected - watch for bearish reversal

"GENUINE BO" (Dark Red): Genuine breakout - bullish continuation likely

"BULLISH" (Lime): Bullish reversal confirmed - strong buy signal

"BEARISH" (Fuchsia): Bearish reversal confirmed - strong sell signal

Trend Column:

"BULL" (Green): EMAs in bullish sequence (20>50>100>200)

"BEAR" (Red): EMAs in bearish sequence (20<50<100<200)

"SIDE" (Gray): Sideways/mixed EMA alignment

Status Column:

"Above 200" (Green): Price above 200 EMA - bullish bias

"Below 200" (Red): Price below 200 EMA - bearish bias

"At 200" (Gray): Price at 200 EMA - neutral

💡 Trading Strategies

Strategy 1: Fake Signal Reversal Trading

For Long Entries (Fake Breakdown Reversal):

Wait for fake breakdown signal (orange triangle down)

Confirm bullish reversal (lime triangle up) when price reclaims EMAs

Enter long on bullish reversal confirmation

Stop loss below the swing low that validated the fake breakdown

Target next resistance level or previous swing high

For Short Entries (Fake Breakout Reversal):

Wait for fake breakout signal (orange triangle up)

Confirm bearish reversal (fuchsia triangle down) when price falls below EMAs

Enter short on bearish reversal confirmation

Stop loss above the swing high that validated the fake breakout

Target next support level or previous swing low

Strategy 2: Genuine Signal Trend Following

For Trend Continuation Longs:

Identify genuine breakout (dark red triangle up)

Confirm higher timeframe alignment (4H/1D showing bullish trend)

Enter on pullback to broken resistance (now support)

Stop loss below the validation swing high

Target measured move or next major resistance

For Trend Continuation Shorts:

Identify genuine breakdown (red triangle down)

Confirm higher timeframe alignment (4H/1D showing bearish trend)

Enter on pullback to broken support (now resistance)

Stop loss above the validation swing low

Target measured move or next major support

Strategy 3: Multi-Timeframe Confluence

High-Probability Setups:

Align signals across timeframes (15M signal + 4H trend confirmation)

Look for confluence (multiple timeframes showing same signal type)

Prioritize higher timeframe signals for swing/position trades

Use lower timeframes for precise entry timing

⚠️ Risk Management Rules

Position Sizing:

Fake signal trades: Reduce position size (higher risk, higher reward)

Genuine signal trades: Standard position size (trend following)

Multi-timeframe confluence: Increase position size (higher probability)

Stop Loss Guidelines:

Fake breakdown longs: Stop below validation swing low

Fake breakout shorts: Stop above validation swing high

Genuine signals: Stop beyond the MA that was broken

Reversals: Stop beyond the reversal invalidation level

Take Profit Strategies:

Scale out at key resistance/support levels

Trail stops using the 20 EMA for trend following

Take partial profits at 1:2 risk/reward ratio

Let winners run on strong trend continuation signals

🔧 Best Practices

Signal Validation:

Wait for candle close before acting on signals

Check volume confirmation on breakouts/breakdowns

Consider market context (news, earnings, etc.)

Avoid trading during low liquidity periods

Timeframe Selection:

Scalping: 15M signals with 4H trend filter

Day Trading: 4H signals with 1D trend filter

Swing Trading: 1D signals with 1W trend filter

Position Trading: 1W signals for major moves

Market Conditions:

Trending Markets: Focus on genuine signals for continuation

Range-Bound Markets: Focus on fake signals for reversals

High Volatility: Reduce position sizes and widen stops

Low Volatility: Look for breakout setups with volume

📋 Advanced Tips

Signal Evolution Monitoring:

Watch for signal transitions (fake becoming genuine or vice versa)

Adjust positions when signal classification changes

Use alerts to stay informed of signal updates

Monitor multiple timeframes for comprehensive analysis

Confluence Factors:

Support/Resistance levels at signal points

Volume spikes on genuine signals

RSI divergences with fake signals

Fibonacci retracements at reversal points

Common Pitfalls to Avoid:

Don't chase signals after significant moves

Don't ignore higher timeframe trends

Don't overtrade on every signal

Don't neglect risk management rules

🎯 Quick Reference

Bullish Signals Priority:

Bullish Reversal (Lime) - Highest priority

Fake Breakdown (Orange) - High probability reversal

Genuine Breakout (Dark Red) - Trend continuation

Bearish Signals Priority:

Bearish Reversal (Fuchsia) - Highest priority

Fake Breakout (Orange) - High probability reversal

Genuine Breakdown (Red) - Trend continuation

Multi-Timeframe Hierarchy:

1W: Major trend direction

1D: Intermediate trend and swing levels

4H: Short-term trend and entry timing

15M: Precise entry and exit points

⚡ Pro Tip: The most powerful signals occur when fake signals reverse into genuine signals in the opposite direction, creating high-momentum moves with excellent risk/reward ratios.

Disclaimer: This indicator is for educational purposes. Always combine with proper risk management, additional technical analysis, and fundamental research before making trading decisions. Past performance does not guarantee future results.

Tight Range Display with Background🌟 Tight Range Transparency Display with Background

What Is This Indicator?

Hey traders! Ever wanted a simple way to spot those quiet, low-volatility moments in the market that often signal a big move is coming? The Tight Range Transparency Display with Background does exactly that! This indicator highlights periods where the price is moving in a tight range—think of it as the calm before the storm. It paints the chart background blue to show these zones, with the shade getting darker the tighter the range becomes. It’s like having a visual cue to say, “Hey, something might be brewing here!”

Why You’ll Love It

Spot Key Moments Easily: The blue background makes it super easy to see when the market is in a tight range, which often happens before breakouts or big trends.

Customizable Settings: You can tweak the range thresholds to match your trading style—whether you’re looking for super tight zones or slightly broader ones.

Visual Clarity: The background gets darker when the range is tighter, giving you a quick sense of how compressed the price action is.

Perfect for Any Market: Works on stocks, forex, crypto, or any chart you trade, across any timeframe.

How to Use It

Add It to Your Chart:

Just copy this script into TradingView’s Pine Editor and hit "Add to Chart." It’ll overlay right on your price chart.

Tweak the Settings:

Open the indicator settings and use the dropdown menus to pick your preferred "Tight Range %" and "Wide Range %." For example, set a Tight Range % of 2.0% to catch smaller ranges, or go higher like 10.0% for broader ones.

You can also adjust the ATR Period (default is 5) to make the indicator more or less sensitive to recent price swings.

Watch for the Blue Background:

When the price enters a tight range, the chart background turns blue. The darker the blue, the tighter the range—meaning a potential breakout could be closer!

Trade Smarter:

Use these tight range zones to prepare for potential breakouts. For example, if you see a dark blue background, it might be a good time to watch for a big price move.

Pair this with other tools like support/resistance levels or volume spikes to confirm your trades.

Who Is This For?

Swing Traders: Perfect for spotting consolidation zones before a big swing.

Breakout Traders: Tight ranges often lead to breakouts—use this to time your entries.

Smart Money Followers: If you’re into smart money concepts, tight ranges can signal accumulation or distribution phases.

Beginners & Pros Alike: It’s easy to use for new traders but powerful enough for seasoned pros.

Real-World Example

Imagine you’re trading a stock on a 1-hour chart. You notice the background turns blue, and it’s getting darker over a few bars. This tells you the price range is tightening—maybe the stock is consolidating after a big move. You check your other indicators, see a volume spike, and spot a breakout above resistance. Boom! You catch the next big trend, all because this indicator helped you focus on the right moment.

Tips for Best Results

Try Different Timeframes: Tight ranges on a 15-minute chart might signal short-term moves, while a daily chart could highlight bigger trends.

Adjust for Your Market: For volatile markets like crypto, you might want a higher Tight Range % (e.g., 10.0%). For calmer markets like forex, try a lower setting (e.g., 2.0%).

Combine with Other Tools: Use this alongside trendlines, moving averages, or volume indicators to confirm your setups.

Why I Made This

I created this indicator because I wanted a simple, visual way to spot those critical low-volatility zones without cluttering my chart. The dynamic background color makes it intuitive to see when the market is “coiling up” for a potential move. I hope it helps you find better trading opportunities just like it does for me!

Let’s Connect

If you find this indicator helpful, I’d love to hear about it! Drop a comment or a rating to let me know how it’s working for you. Got ideas to make it even better? Feel free to message me on TradingView—I’m always open to suggestions.

Published On

Date: May 22, 2025

Happy trading, and may your charts always be in your favor! 🚀

How to Publish on TradingView

Open Pine Editor:

On TradingView, open a chart and go to the Pine Editor tab at the bottom.

Paste the Code:

Copy the script you provided and paste it into the Pine Editor.

Compile:

Click "Add to Chart" to ensure it compiles without errors.

Publish:

Click the "Publish Script" button (paper plane icon) in the Pine Editor.

Select "Publish New Script."

Add the Description:

Title: "Tight Range Transparency Display with Background"

Description: Copy the content above into the description field.

Visibility: Choose "Public" to share with everyone (or "Invite-Only" for restricted access).

Tags: Add tags like "tight range", "breakout", "smart money", "volatility", "swing trading".

Screenshot: Add a screenshot of the indicator on a chart, showing the blue background during a tight range.

Submit:

Click "Publish" to submit. TradingView will review it and make it live if it meets their guidelines.

Additional Notes

Screenshot Tip: Use a chart where the blue background is clearly visible (e.g., during a consolidation period) to make the indicator’s effect stand out.

Engage with Users: After publishing, respond to comments and feedback to build a positive reputation on TradingView.

This content is designed to be approachable and engaging, helping traders understand the value of your indicator and encouraging them to try it out.

0x278's Swing-Failure-Pattern (SFP)0x278's Swing-Failure-Pattern (SFP) ‑ Confirmed Short

Table of Contents

Introduction

Core Concept – What Is an SFP?

How the Indicator Works

Visual Elements & Their Meaning

Input Parameters Explained

Step-by-Step Trading Playbook

Example Workflow (Daily BTC-USDT)

Alerts & Automation

Tips, Tricks & Best Practices

FAQ

Advanced Configuration & Asset-Class Playbook

1. Introduction

The Swing-Failure-Pattern (SFP) – Confirmed Short indicator spots and tracks bearish SFPs on any market and timeframe, with defaults tuned for Daily charts.

A bearish SFP occurs when price sweeps a prior swing high (liquidity grab) and then decisively rejects lower , signalling a possible trend reversal or sharp pullback.

This script automatically:

Identifies the liquidity sweep & rejection (‐"SFP-SHORT" label)

Confirms directional intent via a structure-breaking close below the setup low

Paints a preferred sell-on-retest zone and tracks its validity

Identifies optimal entry opportunities when price retests the zone

Generates optional retest and entry alerts when trading conditions appear

Self-cleans after a configurable number of bars – keeping your chart tidy

Default Timeframe : Daily

Default Market : Crypto / FX majors

Works On : All symbols + timeframes – simply adjust parameters.

2. Core Concept – What Is an SFP?

Sweep (Liquidity Grab) – Price trades above a meaningful swing high, triggering stops & inducing breakout buyers.

Rejection – The same bar (or the next) closes back below the swept high, invalidating the breakout.

Structure Break – Bears confirm intent by closing below the "setup low" (the most recent pivot low before the sweep).

Retest – Price retraces to the sweep zone. Traders seek entries inside the upper half of that zone with invalidation just above the swing high.

The indicator encodes these four steps so you can spot high-quality bearish reversals without manual bar-by-bar analysis.

3. How the Indicator Works

Phase: Sweep & Rejection

Script Logic: high > lastSwingHigh and close < lastSwingHigh

Visual Cue: Red SFP-SHORT label above candle

Phase: Structure Break

Script Logic: Close < setupLow while pattern locked

Visual Cue: Zone (red line-box) plotted; SFP-SHORT label stays

Phase: Retest Tracking

Script Logic: Zone stays active for retestExpiry bars or until tapped

Visual Cue: Orange SFP-RETEST label when hit

Phase: Entry Signal

Script Logic: Price rejection within retest zone

Visual Cue: Green ENTRY label at optimal entry point

Phase: Expiry / Cleanup

Script Logic: Zone deleted after expiry

Visual Cue: Labels fade but remain visible for reference

All calculations reset after each completed/expired pattern ensuring fresh, uncluttered signals.

4. Visual Elements & Their Meaning

SFP-SHORT (red) – Bar that swept a prior high and closed below it.

Red Box / Line – Preferred sell zone between the swing high (upper bound) and dynamic lower bound (see sizing methods). Extends right until filled/expired.

SFP-RETEST (orange) – Bar that first tags the zone after confirmation.

ENTRY (green) – Appears when a high-probability entry signal occurs within the retest zone.

EXPIRED (gray) – Appears when the retest zone expires without being hit.

Visual Persistence – Labels fade but remain visible after expiry for reference and historical analysis.

5. Input Parameters Explained

Pivot Detection

Pivot left / right : Bars left/right of the pivot that must stay below/above it. Tip : Symmetrical values (3/3) work best for clean structure.

Retest Management

Retest expiry (bars) : Lifespan of a retest zone before it is considered stale. Default: 14 bars on Daily . Tip : Shorten for intraday, lengthen for swing trading.

Retest Zone Sizing

Sizing method : Select Static %, ATR-based or Hybrid logic for the lower boundary. Tip : Hybrid balances tight stops with realistic fills.

Static % : Fixed fraction of sweep range when Static/Hybrid is selected. Tip : Higher % deepens zone & widens stop.

ATR period : Look-back length for ATR when volatility sizing is used. Tip : Increase to smooth choppy markets.

ATR multiplier : Multiplier applied to ATR in ATR-based/Hybrid mode. Tip : Higher value widens zone during volatility.

Visual – Retest Zone

Show retest zone box : Toggles drawing of the semi-transparent sell zone box. Tip : Disable for ultra-clean look.

Retest box color : Fill colour of the box (alpha = transparency). Tip : Match your chart theme.

Max retest boxes : How many historical boxes remain visible (0 = unlimited). Tip : Lower to boost performance.

Only show active boxes : Automatically deletes a box once it's hit. Tip : Reduces clutter during back-testing.

Visual – General

Minimal mode : Hides most visuals apart from critical labels. Tip : Ideal for screenshots.

Show retest zone line : Draws a vertical line linking upper/lower boundaries. Tip : Acts as a quick depth guide.

Show ENTRY labels : Plots 'ENTRY' on optimal candles. Tip : Turn off for manual confirmation.

Labels

Label size : Overall size of all labels. Tip : tiny / small / normal.

Use simple label style : Switches to pixel text style for labels. Tip : Faster rendering on low-spec machines.

Advanced

minPct / maxPct (hard-coded) : Internal floor/cap for Hybrid logic. Tip : Exposed in code for power-users only.

Zone-Sizing Methods

Static – Lower bound = sweepRange × staticPct.

ATR-based – Lower bound = ATR × multiplier, normalised to the sweepRange.

Hybrid – Uses the greater of Static and ATR-based (capped by an internal safety ceiling).

6. Step-by-Step Trading Playbook

Identify Context – Prefer setups against extended moves into obvious highs (e.g., daily swing highs, prior week high, round numbers).

Wait for SFP Confirmation – The indicator will label an SFP-SHORT only after the candle closes. Do not front-run.

Structure-Break Close – A close below setupLow turns the zone live. This is your go signal – prepare sell orders.

Place Orders in the Zone

Entry : Limit order anywhere between retestLower and the swing high.

Stop : 1-2 ticks/pips above the swing high.

Risk Management

Size position so risk per trade ≤ account risk % (common: 0.5-1%).

If no retest before retestExpiry bars → cancel order .

Targets

Conservative: First liquidity pocket / FVG below.

Aggressive: 2-3× risk or next HTF support.

Trail or Partial – Consider trailing stop once 1R is achieved or partial profit at 1R.

7. Example Workflow (Daily BTC-USDT)

BTC trades to a fresh one-month high at $31 050 sweeping prior highs.

Candle closes at $30 420 – below the swept high – SFP-SHORT label appears.

Two days later, candle closes below setupLow at $29 880 – confirmation & zone plotted (upper = $31 050, lower ≈ $30 550).

Five days later price retests the zone hitting $30 750 – SFP-RETEST alert fires, trade filled.

Stop placed @ $31 120 (70$ risk). 1R target = $29 680 reached four days later.

8. Alerts & Automation

SFP Short confirmed

Fires When: Structure-break close below setupLow.

Suggested Action: Prepare/submit sell-limit order in the zone.

SFP Short retest

Fires When: Price enters the retest zone.

Suggested Action: Monitor for entry signals or prepare for manual entry.

SFP Short Entry Signal

Fires When: Optimal entry conditions detected within retest zone.

Suggested Action: Execute short trade with defined risk parameters.

Use TradingView's Webhook URL to forward alerts to a trade-execution bot (e.g., PineConnector) for automated order placement.

9. Tips, Tricks & Best Practices

Combine with HTF Bias – Only take bearish SFPs in bearish weekly trend.

Watch Volume – High volume on the sweep bar adds conviction.

Time Window – SFPs during NY session FX / US session crypto tend to be stronger.

Cluster Zones – Multiple overlapping SFP zones increase probability; treat the cluster as one larger supply.

Avoid News – Skip SFPs forming minutes before high-impact macro news.

10. FAQ

Q: Can I use this on lower timeframes?

A: Yes – reduce retestExpiry (e.g., 15 bars on 15-minute) and test ATR-based sizing.

Q: Does it work for longs?

A: This script focuses on bearish SFPs. Clone & invert conditions for longs.

Q: Why did a zone disappear?

A: Either it expired (retestExpiry) without a retest or the cleanup routine removed old visuals to stay within Pine limits (500 objects per type).

Q: What's the difference between the "SFP-RETEST" and "ENTRY" signals?

A: "SFP-RETEST" indicates price has entered the zone, while "ENTRY" signals an optimal entry opportunity based on price rejection within the zone.

Q: How do I customize the label appearance?

A: Use the "Label size" and "Use simple label style" settings to adjust all labels to your preferred visual style.

Happy trading & trade safe!

11. Advanced Configuration & Asset-Class Playbook

Why does the retest box feel "too high" and how do I actually get filled? Use the quick tweaks below or the power-user code snippet to shape the zone to your personality and instrument.

11.1 Why the default box is shallow

The Static 25 % / ATR-Hybrid logic keeps stops small. Around 50 % of Daily BTC SFPs never look back – that's the cost of tight risk. If you need higher fill-rates, deepen the zone (11.2).

11.2 Three slider moves – no coding required

Retest zone sizing method – switch Static → Hybrid or ATR-based

Static % – raise from 0.25 → 0.45-0.60

ATR multiplier – raise from 1.0 → 1.5-2.0

Each turn pulls the lower edge of the box deeper while keeping the invalidation at the swing high.

11.3 One-liner for coders

To allow >60 % of the sweep range edit the source:

Old code:

minPct = 0.05

maxPct = 0.60

New code:

minPct = 0.05

maxPct = input.float(0.60, "Max retest % of sweep", step = 0.05, minval = 0.10, maxval = 0.95)

Then dial the cap up to ~0.80-0.90 from the settings panel.

11.4 If price never comes back…

No-retest partial – take 25-40 % size on the confirmation candle, stop above the high.

Lower-TF confirmation – drop to 4 h / 1 h and hunt an internal SFP or bearish FVG inside the sweep.

ATR trail – if price dumps immediately, trail the stop above each new lower-high.

11.5 Asset-Class Cheat-Sheet

Crypto – Daily : Static %: 0.20-0.35, ATR mult: 1.0, Retest Expiry: 12-20 . Notes : High volatility; sweeps expand fast.

FX Majors – 4 h/D : Static %: 0.25-0.40, ATR mult: 1.2, Retest Expiry: 15-25 . Notes : ATR handles session compression.

Index Futures – 1 h : Static %: 0.30-0.50, ATR mult: 1.5, Retest Expiry: 10-20 . Notes : Hybrid recommended; gaps tighten sweeps.

US Equities – 30 m : Static %: 0.35-0.55, ATR mult: 1.5-2.0, Retest Expiry: 10-14 . Notes : Consider no-retest entry on earnings spikes.

Always forward-test on your own symbol & timeframe ✔️

AxisAxis Indicator: Dynamic Trend Lines & Support/Resistance with Trading Mode Presets

Overview

The Axis indicator is a powerful, all-in-one tool for traders, designed to identify key trend lines and support/resistance (S&R) levels across various trading strategies. With 11 predefined trading modes—Scalping, Day Trading, Swing Trading, Long-Term, Position Trading, Breakout Trading, Mean Reversion, Trend Following, Range Trading, Volatility Trading, and Counter-Trend Trading—Axis adapts to your trading style by automatically adjusting parameters like volume Moving Average (MA) periods, fractal lookbacks, and alert proximity. Built-in timeframe validation ensures you’re using the optimal chart timeframe for your selected mode, with a warning label displayed if the timeframe is unsuitable. Whether you’re a scalper chasing quick moves or a position trader eyeing long-term trends, Axis provides precise, volume-filtered signals to enhance your trading decisions.

How It Works

Axis plots two sets of trend lines (A and B) and two sets of S&R levels (A and B) on your chart, each tailored to the selected trading mode:

Trend Lines (A & B): Identifies uptrend and downtrend lines using pivot highs/lows with mode-specific lookback periods. Lines are drawn only when volume exceeds the mode’s volume MA, ensuring high-probability signals.

Support/Resistance (A & B): Plots horizontal S&R levels based on pivot highs/lows, filtered by volume to highlight significant price levels.

Volume MA: Uses a mode-specific MA type (SMA, EMA, WMA, HMA, or VWMA) to validate pivots. MA periods are scaled by timeframe (e.g., 1m, 1h, Daily) and capped at 5,000 candles to prevent errors.

Timeframe Validation: Checks if the chart’s timeframe matches the mode’s recommended range (e.g., 5m–1h for Volatility Trading). If not, a yellow warning label appears (e.g., “Timeframe may not suit Scalping”).

Alerts: Triggers alerts for new trend lines, S&R levels, and price crosses, allowing real-time trade monitoring.

Trading Modes & Recommended Timeframes

Each mode is preconfigured with optimized settings for specific strategies and timeframes:

Scalping (1m–15m): Fast signals with short lookbacks (1–3 bars) and tight alerts (0.2%) for intraday scalps.

Day Trading (15m–1h): Intraday focus with moderate lookbacks (2–4 bars) and 0.3% alert proximity.

Swing Trading (1h–4h): Multi-day/week trades with balanced settings (2–5 bars, 0.5% alerts).

Long-Term (Daily–Weekly): Major trends with longer lookbacks (3–7 bars, 1.0% alerts).

Position Trading (Weekly–Monthly): Long-term moves with robust settings (4–20 bars, 1.5% alerts).

Breakout Trading (30m–4h): Detects breakouts with sensitive settings (1–4 bars, 0.25% alerts).

Mean Reversion (1h–Daily): Targets reversals with moderate settings (3–8 bars, 0.7% alerts).

Trend Following (4h–Weekly): Captures trends with longer lookbacks (4–18 bars, 1.2% alerts).

Range Trading (1h–4h): Optimized for consolidation with balanced settings (2–6 bars, 0.4% alerts).

Volatility Trading (5m–1h): High-volatility markets with ultra-sensitive settings (1–2 bars, 0.15% alerts).

Counter-Trend Trading (4h–Daily): Contrarian reversals with robust settings (3–9 bars, 0.9% alerts).

Key Features

11 Trading Modes: Preconfigured settings for diverse strategies, eliminating manual tuning.

Dynamic Volume MA: Supports SMA, EMA, WMA, HMA, and VWMA, scaled by timeframe for accuracy.

Timeframe Validation: Warns if the chart timeframe doesn’t suit the mode, preventing suboptimal setups.

Customizable Visuals: Adjust line widths and colors for trend lines and S&R levels.

Comprehensive Alerts: Alerts for new trend lines, S&R levels, and price crosses, integrable with TradingView’s alert system.

Performance Optimized: MA periods capped at 5,000 candles to avoid errors and ensure smooth operation.

How to Use

Add to Chart: Apply the Axis indicator to your TradingView chart.

Select Trading Mode: Choose a mode from the “Trading Mode” dropdown in the indicator settings (e.g., Volatility Trading for crypto on 5m).

Check Timeframe: Ensure your chart’s timeframe matches the mode’s recommended range (e.g., 5m–1h for Volatility Trading). A yellow warning label appears if the timeframe is unsuitable.

Customize Visuals: Adjust line widths and colors for trend lines (A & B) and S&R (A & B) in the settings.

Set Alerts: Create alerts for new trend lines, S&R levels, or price crosses via TradingView’s alert menu.

Trade Signals:

Trend Lines: Use uptrend/downtrend lines for trend confirmation or breakout setups.

S&R Levels: Trade bounces or breaks at support/resistance, confirmed by volume.

Alerts: Act on price cross alerts for entries/exits based on your strategy.

Tips for Best Results

Match Timeframe to Mode: Stick to recommended timeframes (e.g., 1h–4h for Swing Trading) to maximize signal accuracy. Heed warning labels for timeframe mismatches.

Test Across Assets: Volatility Trading shines in crypto during news events, while Range Trading suits forex/stocks in consolidation.

Backtest Strategies: Convert Axis to a strategy (e.g., enter on S&R cross, exit after X bars) to validate performance.

Optimize for Performance: If lag occurs on low timeframes, reduce the MA cap to 2,500 (edit math.min(..., 2500) in the code).

Combine with Other Tools: Pair Axis with indicators like RSI or MACD for confluence.

Why Choose Axis?

Axis simplifies technical analysis by offering a single indicator that adapts to your trading style. Its mode-based presets, volume-filtered signals, and timeframe validation make it ideal for traders of all levels, from scalpers to long-term investors. Whether you’re trading crypto, forex, or stocks, Axis delivers actionable insights with minimal setup.

Feedback & Support

If you have questions, suggestions, or need help customizing Axis, feel free to comment or contact me via TradingView. Your feedback helps improve the indicator for the community!

Value Scanner | QuantEdgeB📡 Value Scanner | QuantEdgeB

🔍 What is the Value Scanner?

The Value Scanner by QuantEdgeB is a volatility-adaptive valuation framework that dynamically evaluates where price sits relative to a custom “Fair Value” zone. It combines your choice of moving average engine (SMA, WMA, VIDYA, etc.) with multi-layered standard deviation or ATR-based bands to highlight extreme conditions, reversal zones, and statistical overextensions in real time.

💡 Think of Value Scanner as a radar grid, continuously scanning market terrain and painting a full spectrum from balance to extreme disequilibrium.

⚙️ Core Components

✅ Customizable Moving Average Core

At the heart of the scanner lies a flexible moving average engine:

• Choose from 12+ advanced types: 𝓦𝓜𝓐, 𝓥𝓦𝓜𝓐, 𝓥𝓘𝓓𝓨𝓐, 𝓢𝓜𝓜𝓐, 𝓐𝓛𝓜𝓐, 𝓛𝓢𝓜𝓐, and more.

• Fair Value is derived from this base and acts as the center of the statistical zones.

✅ Volatility-Driven Band Construction

Two volatility methods power the adaptive zones:

• Average True Range (ATR): Ideal for reactive, price-based spreads.

• Standard Deviation (SD): Better for modeling reversion and deviation symmetry.

The scanner builds up to ±5σ zones, dynamically updating in real time.

🎯 Signal and Zone Identification

🧭 Deviation Labels

The system assigns a statistical label at every candle:

• From +0.5σ to +5σ for increasing levels of overextension upward.

• From -0.5σ to -5σ for oversold and undervalued conditions.

🌐 Market Stage Detection

Each deviation zone is translated into an intuitive market phrase such as:

• “𝓔𝔁𝓽𝓻𝓮𝓶𝓮𝓵𝔂 𝓞𝓿𝓮𝓻𝓫𝓸𝓾𝓰𝓱𝓽”

• “𝓜𝓲𝓭 𝓥𝓪𝓵𝓾𝓮 / 𝓑𝓪𝓵𝓪𝓷𝓬𝓮𝓭”

• “𝓜𝓪𝔁𝓲𝓶𝓾𝓶 𝓔𝔁𝓽𝓮𝓷𝓼𝓲𝓸𝓷 𝓓𝓸𝔀𝓷”

These phrases help you intuitively gauge risk, reward, and imbalance without needing to study a chart for long.

🔺 Signal Mechanics

📌 Reversal Signals (Optional)

• Automatic buy signals when price crosses above key lower deviation levels.

• Sell signals when price crosses below upper deviation bands.

• Ideal for mean-reversion setups or high-probability reversal plays.

🖼️ Visual Overlay Engine

• Beautifully shaded volatility bands with decreasing opacity as they move away from fair value.

• Background coloring highlights extreme price zones for fast visual alerts.

• Built-in "table display" summarizing the current base, volatility method, direction, fair value, and deviation stage.

📊 Table Overlay Features

The live diagnostic table (position adjustable) displays:

• 📈 Current Base MA Type

• 🌡️ Volatility Method in use (ATR or SD)

• 🧭 Trend direction (rising/falling/neutral)

• 🧮 Current Deviation Label (+2σ, -3σ, etc.)

• 🚦 Interpretive Stage Phrase ("Strongly Overbought", etc.)

• 📍 Real-Time Fair Value

• 🚨 Upper & Lower Extremes

🧠 Why Use the Value Scanner?

This tool is designed for traders who want to:

• Identify price extremes relative to statistical norms.

• Time entries and exits based on price's relationship to value zones.

• Visualize volatility structure without clutter.

• Combine trend-following or mean-reversion logic with elegant overlays and table analytics.

💼 Ideal Use Cases

• Swing trading: Spot overextensions or returns to mean.

• Options traders: Gauge volatility compression or expansion.

• Reversion systems: Generate contrarian signals at edge zones.

• Trend continuation: Use +1σ or -1σ as breakout validation levels.

🧬 Default Settings

• Base Type: 𝓦𝓜𝓐

• Length: 21

• Volatility Type: 𝓐𝓿𝓰. 𝓣𝓻𝓾𝓮 𝓡𝓪𝓷𝓰𝓮

•. Volatility Lengths: ATR 14 / Stdev 30

🧬 In Summary

Value Scanner | QuantEdgeB is not just a volatility band indicator — it’s a contextual market scanner that combines price equilibrium theory with precision deviation mapping. It adds statistical insight, color-coded extremes, and narrative stage identification — all in real time.

Whether you’re trend-following or fading extremes, this system helps you locate value, measure dislocation, and trade with mathematical confidence.

📌 Trade with Statistical Precision | Powered by QuantEdgeB

🔹 Disclaimer: Past performance is not indicative of future results.

🔹 Strategic Advice: Always backtest, optimize, and align parameters with your trading objectives and risk tolerance before live trading.

Enhanced Volume Trend Indicator with BB SqueezeEnhanced Volume Trend Indicator with BB Squeeze: Comprehensive Explanation

The visualization system allows traders to quickly scan multiple securities to identify high-probability setups without detailed analysis of each chart. The progression from squeeze to breakout, supported by volume trend confirmation, offers a systematic approach to identifying trading opportunities.

The script combines multiple technical analysis approaches into a comprehensive dashboard that helps traders make informed decisions by identifying high-probability setups while filtering out noise through its sophisticated confirmation requirements. It combines multiple technical analysis approaches into an integrated visual system that helps traders identify potential trading opportunities while filtering out false signals.

Core Features

1. Volume Analysis Dashboard

The indicator displays various volume-related metrics in customizable tables:

AVOL (After Hours + Pre-Market Volume): Shows extended hours volume as a percentage of the 21-day average volume with color coding for buying/selling pressure. Green indicates buying pressure and red indicates selling pressure.

Volume Metrics: Includes regular volume (VOL), dollar volume ($VOL), relative volume compared to 21-day average (RVOL), and relative volume compared to 90-day average (RVOL90D).

Pre-Market Data: Optional display of pre-market volume (PVOL), pre-market dollar volume (P$VOL), pre-market relative volume (PRVOL), and pre-market price change percentage (PCHG%).

2. Enhanced Volume Trend (VTR) Analysis

The Volume Trend indicator uses adaptive analysis to evaluate buying and selling pressure, combining multiple factors:

MACD (Moving Average Convergence Divergence) components

Volume-to-SMA (Simple Moving Average) ratio

Price direction and market conditions

Volume change rates and momentum

EMA (Exponential Moving Average) alignment and crossovers

Volatility filtering

VTR Visual Indicators

The VTR score ranges from 0-100, with values above 50 indicating bullish conditions and below 50 indicating bearish conditions. This is visually represented by colored circles:

"●" (Filled Circle):

Green: Strong bullish trend (VTR ≥ 80)

Red: Strong bearish trend (VTR ≤ 20)

"◯" (Hollow Circle):

Green: Moderate bullish trend (VTR 65-79)

Red: Moderate bearish trend (VTR 21-35)

"·" (Small Dot):

Green: Weak bullish trend (VTR 55-64)

Red: Weak bearish trend (VTR 36-45)

"○" (Medium Hollow Circle): Neutral conditions (VTR 46-54), shown in gray

In "Both" display mode, the VTR shows both the numerical score (0-100) alongside the appropriate circle symbol.

Enhanced VTR Settings

The Enhanced Volume Trend component offers several advanced customization options:

Adaptive Volume Analysis (volTrendAdaptive):

When enabled, dynamically adjusts volume thresholds based on recent market volatility

Higher volatility periods require proportionally higher volume to generate significant signals

Helps prevent false signals during highly volatile markets

Keep enabled for most trading conditions, especially in volatile markets

Speed of Change Weight (volTrendSpeedWeight, range 0-1):

Controls emphasis on volume acceleration/deceleration rather than absolute levels

Higher values (0.7-1.0): More responsive to new volume trends, better for momentum trading

Lower values (0.2-0.5): Less responsive, better for trend following

Helps identify early volume trends before they fully develop

Momentum Period (volTrendMomentumPeriod, range 2-10):

Defines lookback period for volume change rate calculations

Lower values (2-3): More responsive to recent changes, better for short timeframes

Higher values (7-10): Smoother, better for daily/weekly charts

Directly affects how quickly the indicator responds to new volume patterns

Volatility Filter (volTrendVolatilityFilter):

Adjusts significance of volume by factoring in current price volatility

High volume during high volatility receives less weight

High volume during low volatility receives more weight

Helps distinguish between genuine volume-driven moves and volatility-driven moves

EMA Alignment Weight (volTrendEmaWeight, range 0-1):

Controls importance of EMA alignments in final VTR calculation

Analyzes multiple EMA relationships (5, 10, 21 period)

Higher values (0.7-1.0): Greater emphasis on trend structure

Lower values (0.2-0.5): More focus on pure volume patterns

Display Mode (volTrendDisplayMode):

"Value": Shows only numerical score (0-100)

"Strength": Shows only symbolic representation

"Both": Shows numerical score and symbol together

3. Bollinger Band Squeeze Detection (SQZ)

The BB Squeeze indicator identifies periods of low volatility when Bollinger Bands contract inside Keltner Channels, often preceding significant price movements.

SQZ Visual Indicators

"●" (Filled Circle): Strong squeeze - high probability setup for an impending breakout

Green: Strong squeeze with bullish bias (likely upward breakout)

Red: Strong squeeze with bearish bias (likely downward breakout)

Orange: Strong squeeze with unclear direction

"◯" (Hollow Circle): Moderate squeeze - medium probability setup

Green: With bullish EMA alignment

Red: With bearish EMA alignment

Orange: Without clear directional bias

"-" (Dash): Gray dash indicates no squeeze condition (normal volatility)

The script identifies squeeze conditions through multiple methods:

Bollinger Bands contracting inside Keltner Channels

BB width falling to bottom 20% of recent range (BB width percentile)

Very narrow Keltner Channel (less than 5% of basis price)

Tracking squeeze duration in consecutive bars

Different squeeze strengths are detected:

Strong Squeeze: BB inside KC with tight BB width and narrow KC

Moderate Squeeze: BB inside KC with either tight BB width or narrow KC

No Squeeze: Normal market conditions

4. Breakout Detection System

The script includes two breakout indicators working in sequence:

4.1 Pre-Breakout (PBK) Indicator

Detects potential upcoming breakouts by analyzing multiple factors:

Squeeze conditions lasting 2-3 bars or more

Significant price ranges

Strong volume confirmation

EMA/MACD crossovers

Consistent price direction

PBK Visual Indicators

"●" (Filled Circle): Detected pre-breakout condition

Green: Likely upward breakout (bullish)

Red: Likely downward breakout (bearish)

Orange: Direction not yet clear, but breakout likely

"-" (Dash): Gray dash indicates no pre-breakout condition

The PBK uses sophisticated conditions to reduce false signals including minimum squeeze length, significant price movement, and technical confirmations.

4.2 Breakout (BK) Indicator

Confirms actual breakouts in progress by identifying:

End of squeeze or strong expansion of Bollinger Bands

Volume expansion

Price moving outside Bollinger Bands

EMA crossovers with volume confirmation

MACD crossovers with significant price range

BK Visual Indicators

"●" (Filled Circle): Confirmed breakout in progress

Green: Upward breakout (bullish)

Red: Downward breakout (bearish)

Orange: Unusual breakout pattern without clear direction

"◆" (Diamond): Special breakout conditions (meets some but not all criteria)

"-" (Dash): Gray dash indicates no breakout detected

The BK indicator uses advanced filters for confirmation:

Requires consecutive breakout signals to reduce false positives

Strong volume confirmation requirements (40% above average)

Significant price movement thresholds

Consistency checks between price action and indicators

5. Market Metrics and Analysis

Price Change Percentage (CHG%)

Displays the current percentage change relative to the previous day's close, color-coded green for positive changes and red for negative changes.

Average Daily Range (ADR%)

Calculates the average daily percentage range over a specified period (default 20 days), helping traders gauge volatility and set appropriate price targets.

Average True Range (ATR)

Shows the Average True Range value, a volatility indicator developed by J. Welles Wilder that measures market volatility by decomposing the entire range of an asset price for that period.

Relative Strength Index (RSI)

Displays the standard 14-period RSI, a momentum oscillator that measures the speed and change of price movements on a scale from 0 to 100.

6. External Market Indicators

QQQ Change

Shows the percentage change in the Invesco QQQ Trust (tracking the Nasdaq-100 Index), useful for understanding broader tech market trends.

UVIX Change

Displays the percentage change in UVIX, a volatility index, providing insight into market fear and potential hedging activity.

BTC-USD

Shows the current Bitcoin price from Coinbase, useful for traders monitoring crypto correlation with equities.

Market Breadth (BRD)

Calculates the percentage difference between ATHI.US and ATLO.US (high vs. low securities), indicating overall market direction and strength.

7. Session Analysis and Volume Direction

Session Detection

The script accurately identifies different market sessions:

Pre-market: 4:00 AM to 9:30 AM

Regular market: 9:30 AM to 4:00 PM

After-hours: 4:00 PM to 8:00 PM

Closed: Outside trading hours

This detection works on any timeframe through careful calculation of current time in seconds.

Buy/Sell Volume Direction

The script analyzes buying and selling pressure by:

Counting up volume when close > open

Counting down volume when close < open

Tracking accumulated volume within the day

Calculating intraday pressure (up volume minus down volume)

Enhanced AVOL Calculation

The improved AVOL calculation works in all timeframes by:

Estimating typical pre-market and after-hours volume percentages

Combining yesterday's after-hours with today's pre-market volume

Calculating this as a percentage of the 21-day average volume

Determining buying/selling pressure by analyzing after-hours and pre-market price changes

Color-coding results: green for buying pressure, red for selling pressure

This calculation is particularly valuable because it works consistently across any timeframe.

Customization Options

Display Settings

The dashboard has two customizable tables: Volume Table and Metrics Table, with positions selectable as bottom_left or bottom_right.

All metrics can be individually toggled on/off:

Pre-market data (PVOL, P$VOL, PRVOL, PCHG%)

Volume data (AVOL, RVOL Day, RVOL 90D, Volume, SEED_YASHALGO_NSE_BREADTH:VOLUME )

Price metrics (ADR%, ATR, RSI, Price Change%)

Market indicators (QQQ, UVIX, Breadth, BTC-USD)

Analysis indicators (Volume Trend, BB Squeeze, Pre-Breakout, Breakout)

These toggle options allow traders to customize the dashboard to show only the metrics they find most valuable for their trading style.

Table and Text Customization

The dashboard's appearance can be customized:

Table background color via tableBgColor

Text color (White or Black) via textColorOption

The indicator uses smart formatting for volume and price values, automatically adding appropriate suffixes (K, M, B) for readability.

MACD Configuration for VTR

The Volume Trend calculation incorporates MACD with customizable parameters:

Fast Length: Controls the period for the fast EMA (default 3)

Slow Length: Controls the period for the slow EMA (default 9)

Signal Length: Controls the period for the signal line EMA (default 5)

MACD Weight: Controls how much influence MACD has on the volume trend score (default 0.3)

These settings allow traders to fine-tune how momentum is factored into the volume trend analysis.

Bollinger Bands and Keltner Channel Settings

The Bollinger Bands and Keltner Channels used for squeeze detection have preset (hidden) parameters:

BB Length: 20 periods

BB Multiplier: 2.0 standard deviations

Keltner Length: 20 periods

Keltner Multiplier: 1.5 ATR

These settings follow standard practice for squeeze detection while maintaining simplicity in the user interface.

Practical Trading Applications

Complete Trading Strategies

1. Squeeze Breakout Strategy

This strategy combines multiple components of the indicator:

Wait for a strong squeeze (SQZ showing ●)

Look for pre-breakout confirmation (PBK showing ● in green or red)

Enter when breakout is confirmed (BK showing ● in same direction)

Use VTR to confirm volume supports the move (VTR ≥ 65 for bullish or ≤ 35 for bearish)

Set profit targets based on ADR (Average Daily Range)

Exit when VTR begins to weaken or changes direction

2. Volume Divergence Strategy

This strategy focuses on the volume trend relative to price:

Identify when price makes a new high but VTR fails to confirm (divergence)

Look for VTR to show weakening trend (● changing to ◯ or ·)

Prepare for potential reversal when SQZ begins to form

Enter counter-trend position when PBK confirms reversal direction

Use external indicators (QQQ, BTC, Breadth) to confirm broader market support

3. Pre-Market Edge Strategy

This strategy leverages pre-market data:

Monitor AVOL for unusual pre-market activity (significantly above 100%)

Check pre-market price change direction (PCHG%)

Enter position at market open if VTR confirms direction

Use SQZ to determine if volatility is likely to expand

Exit based on RVOL declining or price reaching +/- ADR for the day

Market Context Integration

The indicator provides valuable context for trading decisions:

QQQ change shows tech market direction

BTC price shows crypto market correlation

UVIX change indicates volatility expectations

Breadth measurement shows market internals

This context helps traders avoid fighting the broader market and align trades with overall market direction.

Timeframe Optimization

The indicator is designed to work across different timeframes:

For day trading: Focus on AVOL, VTR, PBK/BK, and use shorter momentum periods

For swing trading: Focus on SQZ duration, VTR strength, and broader market indicators

For position trading: Focus on larger VTR trends and use EMA alignment weight

Advanced Analytical Components

Enhanced Volume Trend Score Calculation

The VTR score calculation is sophisticated, with the base score starting at 50 and adjusting for:

Price direction (up/down)

Volume relative to average (high/normal/low)

Volume acceleration/deceleration

Market conditions (bull/bear)

Additional factors are then applied, including:

MACD influence weighted by strength and direction

Volume change rate influence (speed)

Price/volume divergence effects

EMA alignment scores

Volatility adjustments

Breakout strength factors

Price action confirmations